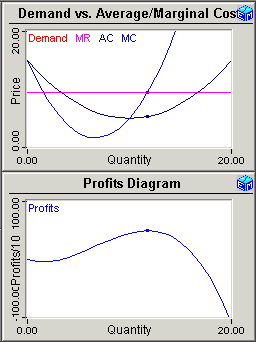

The Perfect Competition application first draws and explains the origins of (a) the average cost curve, (b) the marginal cost curve, (c) the demand curve, and (d) the marginal revenue curve.

![]() Model Link: Perfect

Competition

Model Link: Perfect

Competition

<activate

the model links>

Printable PDF Exercises

Q: When is MC is above AC, below AC, and equal to AC?

Q: When is MC is above AC, below AC, and equal to AC?

The next step is to find the profit-maximizing position. You adjust the quantity produced manually to see first-hand how a firm facing a horizontal demand curve maximizes profits by producing where the marginal cost equals the market price. You then use a built-in iterative procedure to automatically maximize profits.

Movie: Perfect Competition

(40 seconds)

To illustrate the behavior of the firm in a changing environment, you study how the profit maximizing quantity changes when changes in technology shift the average cost and marginal cost curves.

Classic Economic Models

Microeconomics

Introduction

Overview of Micro Models

Supply and Demand

Basic Supply and Demand

Who Pays a Sales Tax?

The Cobweb Model and

Inventory-Based Pricing

Theory of the Firm

Perfect Competition

Monopoly and

Monopolistic Competition

Price Discrimination

The Demand for Labor

Theory of the Consumer

Two Goods - Two Prices

Intertemporal Substitution

Labor Supply, Income Taxes,

and Transfer Payments

Macroeconomics

Introduction

Overview of Macro Models

Models in Chronological Order

The Classical Model

The Simple Keynesian Model

The Keynesian IS/LM Model

The Mundell-Fleming Model

Real Business Cycles

The IS/MP Model

The Solow Growth Model

Financial Markets

Utility-Based Valuation of Risk

Mean-Variance Analysis:

Risk vs. Expected Return

Fixed Income Securities:

Mortgage/Bond Calculator

Growth Investments:

Present Value Calculator

Resources